Hats off to whoever made this. It sums up the whole real estate ridiculousness of the past few years quite nicely.

Monday, December 31, 2007

Wednesday, December 26, 2007

Wednesday, December 19, 2007

The Clinton Housing Bubble

It is comforting to know there are brilliant guys (nobel prize winner in Economics - 2002) who see the light. If I were really that vain, I'd say he reads my blog. However, all of my arguments are logical, and, if you use logic grounded in reality, as the night follows the day, you will come to the correct conclusions, as Dr. Smith did.

Enjoy,

- eternitus

Enjoy,

- eternitus

The Clinton Housing Bubble

By VERNON L. SMITH

December 18, 2007; Page A20

December 18, 2007; Page A20

The joint housing and mortgage-market crisis once again reminds us that all financial implosions stem from the same cause: borrowing short and lending long without enough equity to weather periodic storms in the gap between.

But this bubble was different. Besides being fueled by housing purchases and repackaged loans, each with inadequate equity -- doubling down with other people's money -- at the end of the capital-gains rainbow was the right to take up to $500,000 of profit, tax free.

Thank you President Bill Clinton for your 1997 action, applauded by the banks, the realtors and all citizens in search of half-millionaire status from an investment they could understand and self deceptively believe to be low risk; thank you for fueling the mother of all housing bubbles; thank you for enabling so many of us who bought second or third homes, and homes before construction began, which we then sold to someone else who dreamed of riches from owning homes long enough to sell to another fool.

Once again, try as we might and in spite of our political rhetoric, we have failed to help the poor in applauding government action intended to help ourselves.

The consumption binge is now over, and there is more than enough blame and souring loans to spread around. Congress, if its members can stop squabbling, wants desperately to sanctify it all with actions sure to launch at some future date the grandmother of all housing and mortgage-market bubbles. This august body has long forgotten that it set the stage for housing bubbles by creating those implicitly taxpayer-backed agencies, Fannie Mae and Freddie Mac, as housing lenders of last resort.

Financial market innovators who invented securitization as a mechanism for creating a liquid national market for mortgages are now criticized for having caused an "agency problem." This is jargon for management not having good incentives to provide investors with "truth in packaging" of the underlying economic risk. But what does truth matter at the height of a bubble? These critics would solve the agency problem with more government regulation. Excuse me, but does not the political process have the biggest agency problem of all?

The Federal Reserve, with a default-risk tiger by the tail, feels handcuffed by its accountability and responsibility for avoiding a cascade of defaults in the highest quality obligations, as well as the bad investments seeking an asymmetric tax-free profit. Shades of Long Term Capital, the Savings and Loan crisis, and heyday of the myth of Portfolio Insurance -- historical cases of borrowing short to lend for what may turn out to be longer than expected. They are all conditioned on the existence of liquidity for sellers that can dry up with frightening speed.

Consequently we have the "independent" Fed being driven by market forces to accommodate the long-evident and glaringly least-defensible features of the housing/mortgage markets. Moreover, the moment the Fed abandoned its stance against inflation, the dollar, gold, oil and commodity prices signaled inflation, and now two months later consumer prices have confirmed the signal.

More daring than the action to exempt real estate from the capital gains tax -- and in lasting service to the poor -- would have been actions allowing capital gains on all assets to go tax free, provided that the capital was reinvested -- i.e., not consumed, and yes, good citizens, housing counts as consumption.

Unlike the latest housing bubble, the stock market "excesses" of the 1990s financed thousands of new ventures, some of which found innovative ways to manage the proliferation of new technologies. The result: astonishing, long-term increases in productivity still evident in the most recent quarter.

Adam Smith in his "The Theory of Moral Sentiments" (1759) saw the subtle truth that consumption by the rich has little effect on the welfare of the poor. That's because the income of the rich is largely invested in the tools and knowledge of production, which provide future long-term value for everyone: "The rich only select from the heap what is most precious and agreeable . . . though they mean only their own conveniency . . . [and] . . . the gratification of their own vain and insatiable desires, they divide with the poor the produce of all their improvements."

Expenditures on housing construction are not "improvements" yielding increased productivity and future new wealth to be divided with the poor. They are more akin to satisfying government-subsidized vanity.

Mr. Smith, a professor of law and economics at George Mason University, is the 2002 Nobel Laureate in economics.

Tuesday, December 18, 2007

Greenspan: Captain Insano

Either Greenspan is suffering from dementia, or he is a nut and we didn't know it all these years because he hardly talked. I'm amazed that he continues to deny responsibility for this mess even though he is obviously at fault. He is simply lying to himself, and if he believes it he's an absolute fool.

Way to continue to damage whatever is left of your legacy, Mr. Greenspan...

I'm not sure I need to say any more about the following.

-eternitus

--------------------------------------------------------------------------------------------

Alan Greenspan appeared on ABC’s This Week and discussed the odds of recession, as well as the merits of helping out stressed homeowners. Here is an excerpted transcript from his appearance:

Way to continue to damage whatever is left of your legacy, Mr. Greenspan...

I'm not sure I need to say any more about the following.

-eternitus

--------------------------------------------------------------------------------------------

Alan Greenspan appeared on ABC’s This Week and discussed the odds of recession, as well as the merits of helping out stressed homeowners. Here is an excerpted transcript from his appearance:

HOST GEORGE STEPHANOPOULOS: Several … say that there is a 50 percent chance of a recession now. Are they right?

GREENSPAN: Well, that the probabilities of a recession have moved up to close to 50 percent — whether it’s above or below is really extraordinarily difficult to tell. I think that’s correct. You know what the real story is, with this extraordinary credit problems we’re confronting, why the probabilities are not 60% or 70%?

STEPHANOPOULOS: Why aren’t they?

GREENSPAN: The reason, which is fascinating, if you look at the data, is that because of the decline in long-term rates, interest rates for a protracted period of time, American business was able to fund … [a] significant part of its short-term liabilities, and take out low-cost, long-term debt. So the debt credit needs as such have not all been all that large, and so with credit tightening, ordinarily historically that would have been a very major problem for the American economy. It is clearly less so today, because consumption expenditures, even though they’re being pressed by rising energy prices, are actually moving at a reasonably good clip, and the economy, even though it is slowing down — and the way I put it going to stall speed. I mean, the rate of growth is getting to levels which are such that like a human — like a human system when you get vulnerable, you essentially are open to shocks of one form or another. In other words, when our immune systems go down, we get all sorts of diseases. The economy is similar to that.

STEPHANOPOULOS: One of the shocks we saw back in 1970 I think for the first time was what became known as stagflation…How worried are you about it right now, and what should policymakers do?

GREENSPAN: Well, I’m most concerned about it, as I point out in my book, in the sense that the period that — the last 20 years or so has been a remarkable period in which — without going into any of the details — because of the tremendous geopolitical shifts that occurred at the end of the Cold War, we’ve had a period of remarkable disinflation. That period is now coming to an end, and the evidence is clearly there in rising export prices coming out of China. It’s coming out — it’s showing up in a slowed rate of productivity growth in the United States and elsewhere, and we are beginning to get not stagflation, but the early symptoms of it.

STEPHANOPOULOS: And what do we do about it?

GREENSPAN: Well, the one thing we can do is to recognize that one of the lessons of the last 20 years especially is that low inflation is the major contributor to economic growth overall, and that fundamentally, inflation must be suppressed. And it’s ultimately the Federal Reserve in this country which is the key architect of doing that, and it’s critically important that the Federal Reserve is allowed politically to do what it has to do to

suppress the inflation rates that I see emerging, not immediately, but clearly over the intermediate and longer term period.

STEPHANOPOULOS: Some have pointed out … now the historic ratio of price of homes to income and rents is about 30 percent higher than it is historically. Does that mean we have that far to fall in the housing market?

GREENSPAN: There’s a big dispute as to what the basic level will turn out to be. In my judgment, the prices will stabilize when the rate of liquidation of this very large overhang of newly built single-family homes is at a maximum. Not when we completely get rid of the excess, but when we are well under way. Then the market will begin to stabilize. And at this stage, there is some evidence that sales of homes, new homes, are beginning to flatten out. … And if we can get a further drop in housing starts and housing construction, we can begin to really liquidate that excess of inventories. When we’ve got that well in hand, then, I think, prices stabilize. And I think the ratios of income to rent to all various

other financial aspects is important but not determinate. There are going to be significant losses [on Subprime and Alt-A mortgages]. And there are loss ranges, now — the minimum, now, is $200 billion. But it’s easy, by some calculations, to get to $400 billion.

STEPHANOPOULOS: That’s enormous.

GREENSPAN: It is enormous — except, we have to remember that, as a result of globalization and this extraordinary growth over the last couple of decades, aggregate amount of what we call arbitragable long-term assets, which is all sorts of financial instruments, are close to $100 trillion. And while $400 billion is a very large number, we have to put it in the context of how much damage it can do in this very huge system.

STEPHANOPOULOS: The political world is now looking at the immediate pain. And Senator Clinton looks — has called for a freeze on foreclosures. Senator Edwards called for a rescue fund to be set up by the government for people who are facing these kind of foreclosures. What do you think about those ideas?

GREENSPAN: It’s important to help those people … without affecting the mortgage rates and without affecting the structure of markets. Cash [from the government] is available and we should use that in larger amounts. … It’s far less damaging to the economy to create a short term fiscal problem, which we would, than to try to fix the prices of homes or interest rates. If you do that, it’ll drag this process out indefinitely.

STEPHANOPOULOS: But by infusing cash, it sounds like you agree, then, with former Treasury secretary Larry Summers, who says that, right now, given this crisis, there has to be a bias toward activism.

GREENSPAN: It depends what you mean by activism. If you mean

doing something that works, absolutely. If you mean doing something just for the sake of perceptions, that’s very costly. I don’t know if [infusing cash] would work, but it would certainly help people — it would help their incomes; it would help their personal state, without affecting the structure of the way markets are behaving and the way adjustment process is going on. It’s very critical that this thing reach a selling climax — if I may put it in other words, exhaust itself. It’s only when the markets are perceived to have exhausted themselves on the downside that they turn. Trying to prevent them from going down just merely prolongs the agony.

Monday, December 10, 2007

Monday, December 3, 2007

Mortgage Madness: What is Wrong with America?

Sometimes, with Louis Armstrong playing in the background, I think about the wonderful country we live in, where our leaders make good decisions, our citizens are free and brave, markets are free and the most deserving receive the greatest reward. God bless America.

Then I wake up... Ladies and gentlemen, our country is nuts. I didn't need any more evidence after I saw a gaggle of house "owners" outside of a Countrywide office protesting because they didn't want to or can't pay their debts. I am dumbstruck that a person who receives hundreds of thousands of dollars to buy something is painted as a victim when he/she doesn't pay the money back. And the lender is the bad guy because... gasp!... he wants to receive interest in an amount that would cover his expected losses. These people with crappy credit histories should feel fortunate to receive credit in the first place. Instead, they feel entitled to the same rates that us borrowers who actually pay our debts receive. This is absolute lunacy.

Note the sign that says "My life is not adjustable... stop adjustable rates." A few questions here: If that is the case, lady, why did you enter into an adjustable rate contract? Would you be protesting to give back all of the capital gains you got because the big bad lender gave you money if the housing market were still hot? Didn't you know your rate would reset and that could cost you money? How is it possible not to know what you are getting into when you enter into a financial obligation for an amount of money equal to 10 or 20 years your annual pay?

I'm willing to bet that most people knew what they were getting into and accepted the risk. When they found out how boneheaded their decision was, they wanted to back out. We are a nation of children, with a profound sense of entitlement and a complete lack of personal responsibility. Unfortunately, we are led by politicians who shamelessly pander to these children.

Rate Freezes and Moratoriums

When I first began writing this over the weekend, I thought that the government was getting on the boneheaded train with a "Mr. Freeze" plan, where Hank Paulson shoots all of the subprime mortgages in the U.S. with a freeze ray and locks their rates in for five years, which would be a total disaster. It turns out that his "plan" is for loan servicers to try to figure out which borrowers cannot afford higher rates, but can afford to stay in debt slavery by paying normal interest rates, and charge them those normal interest rates. Well, I have news for you... The servicers already do this!

Hank Paulson as Mr. Freeze? Not Quite

I'm glad that Hammerin' Hank Paulson realizes that an actual blanket rate freeze is a terrible idea (I think we all know how well price controls work). If lowering rates magically turned subprime borrowers into prime borrowers, well, then everyone would be charged the prime rate. It doesn't work that way. Subprime borrowers are charged higher rates because they tend to default more (a lot more) on their payments than prime borrowers. The high rates make sure I can earn a decent return on my investment after accounting for the high loss rates that I'll sustain by giving money to people with shaky credit histories. Freezing subprime rates at low levels virtually guarantees a loss on investment. With legislation pending in congress that makes the investor liable for "predatory" lending practices even though he never saw or met the borrower (he has to take someone else's word for it) and if the interest rates on loans can be reduced whenever politically expedient, who would ever take on such an investment? Any hope for private sector financing of subprime borrowers (what little is left) would be completely gone. As it stands now, subprime financing won't recover for some time.

I'm glad that Hammerin' Hank Paulson realizes that an actual blanket rate freeze is a terrible idea (I think we all know how well price controls work). If lowering rates magically turned subprime borrowers into prime borrowers, well, then everyone would be charged the prime rate. It doesn't work that way. Subprime borrowers are charged higher rates because they tend to default more (a lot more) on their payments than prime borrowers. The high rates make sure I can earn a decent return on my investment after accounting for the high loss rates that I'll sustain by giving money to people with shaky credit histories. Freezing subprime rates at low levels virtually guarantees a loss on investment. With legislation pending in congress that makes the investor liable for "predatory" lending practices even though he never saw or met the borrower (he has to take someone else's word for it) and if the interest rates on loans can be reduced whenever politically expedient, who would ever take on such an investment? Any hope for private sector financing of subprime borrowers (what little is left) would be completely gone. As it stands now, subprime financing won't recover for some time.We all can see what is going on: Most of the subprime "proposals" are desperate, self-serving attempts to put a floor under house prices, all of which are destined to succumb to economic reality. It all boils down to house owners not wanting to admit that their homes are worth less than they thought, and pandering politicians, who know otherwise, but pander to the house owners nonetheless. Now that the Ponzi scheme is over (they always end), house prices will have to re-set to levels that are affordable to the population, regardless of the amount of foreclosures. Forced sales simply expedite the process. Short-sighted policies, like freezing rates, a moratorium on foreclosures, or expanding the FHA to include ever-riskier borrowers (Yeah, were thinking about eliminating the 3% down payment and raising the loan limit to let the government extend no-money down loans to crummy credits in high priced areas - who do you think is going to pay for that one when they all blow up?) only delay the inevitable, and will end up doing much more harm then good.

-eternitus

Friday, November 23, 2007

Friday, November 16, 2007

A discussion of Ron Paul

I have recently become aware that there are allegations on the internet that Ron Paul is a racist. After examining the facts, I must say that most of the things used to support the allegations were "snippets" compiled by a Democrat running against him in a congressional election in 15 years ago in 1992. As I can't examine the context of the statement or the validity of the claims, I cannot pass judgment, though it would be very easy to. While I generally like "easy," it has become painfully apparent to me in cases of character attacks that easy is often unfair. What I can tell you definitively is that Senator Paul has written several essays on racism in the 15 years since then , including the one below. I'll also take a moment to comment on how certain factions in the media and academia use such "branding" to the general detriment of intelligent dialog.

I do believe that his argument is too simplistic, namely that the "holy grail" solution to racism is "liberty." On the other hand, I don't see anything in the above indicating that Ron Paul is a racist... just that his views on the issue are different that we are used to seeing.

That being said, would it not be easy for someone to turn the above into the sensational headline RON PAUL SUPPORTS DON IMUS? Eventually, Ron Paul could even come to equal Don Imus (just like Finkel and Einhorn... name that movie for 10 points) after enough spin, even though his essay was only in defense of Imus' right to free speech, however unseemly. I support his right to free speech as well. If we don't want to hear it , which I don't(I believe Imus was way, way, way out of line), I can simply switch the station.

Unfortunately, I believe his willingness to broach topics such as those above works against him (as it did with Larry Summers' infamous "genderalization" speech, which resulted in his ouster from Harvard's presidency). The primarily liberal academic elite have worked very hard at making certain stances on topics "off limits" without any further examination required (this is curious for a group whose ideals celebrate diversity and open-mindedness). As a graduate of a very liberal academic institution, I am well aware as to how someone can become "branded" (as a nut, a sexist, basically insert something you wouldn't want to be called in here) in such a way, and how "the establishment," for lack of a better term, can discredit a person a priori, regardless of the logical coherence and intrinsic merit of her views at even the slightest hint that it conflicts with "the rules," as decreed by the liberal elite. In this way we attack the person, and not the argument. Such ad hominem methods, while intellectually dishonest and logically fallacious, seem to work marvelously with the general populace, don't they? An argument is doesn't seem to matter much in the realm of popular opinion after you successfully characterize its author as Hitler.

Examples of how this happens can be found in any discussions on differing aptitudes between ethnic groups, or between the sexes. Despite all of the evidence that some differences exist(I can think of at least one ethnic group that is disproportionately represented in elite levels of athletic competition, for instance), discussions of the sort are quickly dismissed as racist or sexist or otherwise out of line without any further examination. Doing such hinders much academic progress in the world today.

Why should we find out if the arguments have merit when we can storm out of the room in a fit of rage, or simply shut down or switch the topic? Such responses are based on emotion, and not logic. We often hear things that are inconsistent with our beliefs. When faced with such cognitive dissonance, we often choose to discredit the opposing viewpoint even in the face of overwhelming evidence. Stifling progressive debate that we simply "don't like" is an example of this. All of this is an attempt to make it easier for us to sleep at night, assured that our beliefs about the world are correct. Facts be damned.

All of this is not to say that some of us are not truly deserving of the brands that we receive. I find, however, that such brands often are put in place for self-serving reasons... to knock someone down in a furtherance of whatever cause we champion. It is easy to imagine how things that Ron Paul might or might not have said 15 years ago may have ruffled somebody's feathers, giving someone cause to brand him as a racist and allowing us to categorically dismiss his views that are outside of the box, the boundaries of which are determined by the liberal elite. Because I know all too well how this happens, I cannot pass judgment on Ron Paul based on sensationalized snippets that were amassed for political gain. Doing so would be intellectually lazy, and completely unfair to the Senator. However, I would like to hear a credible explanation from him before I resume supporting his candidacy.

-eternitus

For what it's worth, I find it hard to believe that anyone as intelligent as he is can hold any sort of truly racist view. We know that the belief that one person is superior to another based solely on the way he or she appears can not hold up when confronted with reality.

Government and Racism

by Ron Paul

by Ron Paul

The controversy surrounding remarks by talk show host Don Imus shows that the nation remains incredibly sensitive about matters of race, despite the outward progress of the last 40 years. A nation that once prided itself on a sense of rugged individualism has become uncomfortably obsessed with racial group identities.

The young women on the basketball team Mr. Imus insulted are over 18 and can speak for themselves. It’s disconcerting to see third parties become involved and presume to speak collectively for minority groups. It is precisely this collectivist mindset that is at the heart of racism.

It’s also disconcerting to hear the subtle or not-so-subtle threats against free speech. Since the FCC regulates airwaves and grants broadcast licenses, we’re told it’s proper for government to forbid certain kinds of insulting or offensive speech in the name of racial and social tolerance. Never mind the 1st Amendment, which states unequivocally that, “Congress shall make NO law.”

Let’s be perfectly clear: the federal government has no business regulating speech in any way. Furthermore, government as an institution is particularly ill-suited to combating bigotry in our society. Bigotry at its essence is a sin of the heart, and we can’t change people’s hearts by passing more laws and regulations.

In fact it is the federal government more than anything else that divides us along race, class, religion, and gender lines. Government, through its taxes, restrictive regulations, corporate subsidies, racial set-asides, and welfare programs, plays far too large a role in determining who succeeds and who fails in our society. This government "benevolence" crowds out genuine goodwill between men by institutionalizing group thinking, thus making each group suspicious that others are receiving more of the government loot. This leads to resentment and hostility between us.

The political left argues that stringent federal laws are needed to combat racism, even as they advocate incredibly divisive collectivist policies.

Racism is simply an ugly form of collectivism, the mindset that views humans strictly as members of groups rather than individuals. Racists believe that all individuals who share superficial physical characteristics are alike: as collectivists, racists think only in terms of groups. By encouraging Americans to adopt a group mentality, the advocates of so-called "diversity" actually perpetuate racism. Their obsession with racial group identity is inherently racist.

The true antidote to racism is liberty. Liberty means having a limited, constitutional government devoted to the protection of individual rights rather than group claims. Liberty means free-market capitalism, which rewards individual achievement and competence, not skin color, gender, or ethnicity.

More importantly, in a free society every citizen gains a sense of himself as an individual, rather than developing a group or victim mentality. This leads to a sense of individual responsibility and personal pride, making skin color irrelevant. Rather than looking to government to correct our sins, we should understand that racism will endure until we stop thinking in terms of groups and begin thinking in terms of individual liberty.

-----------------------------------------------------------------------------------------------I do believe that his argument is too simplistic, namely that the "holy grail" solution to racism is "liberty." On the other hand, I don't see anything in the above indicating that Ron Paul is a racist... just that his views on the issue are different that we are used to seeing.

That being said, would it not be easy for someone to turn the above into the sensational headline RON PAUL SUPPORTS DON IMUS? Eventually, Ron Paul could even come to equal Don Imus (just like Finkel and Einhorn... name that movie for 10 points) after enough spin, even though his essay was only in defense of Imus' right to free speech, however unseemly. I support his right to free speech as well. If we don't want to hear it , which I don't(I believe Imus was way, way, way out of line), I can simply switch the station.

Unfortunately, I believe his willingness to broach topics such as those above works against him (as it did with Larry Summers' infamous "genderalization" speech, which resulted in his ouster from Harvard's presidency). The primarily liberal academic elite have worked very hard at making certain stances on topics "off limits" without any further examination required (this is curious for a group whose ideals celebrate diversity and open-mindedness). As a graduate of a very liberal academic institution, I am well aware as to how someone can become "branded" (as a nut, a sexist, basically insert something you wouldn't want to be called in here) in such a way, and how "the establishment," for lack of a better term, can discredit a person a priori, regardless of the logical coherence and intrinsic merit of her views at even the slightest hint that it conflicts with "the rules," as decreed by the liberal elite. In this way we attack the person, and not the argument. Such ad hominem methods, while intellectually dishonest and logically fallacious, seem to work marvelously with the general populace, don't they? An argument is doesn't seem to matter much in the realm of popular opinion after you successfully characterize its author as Hitler.

Examples of how this happens can be found in any discussions on differing aptitudes between ethnic groups, or between the sexes. Despite all of the evidence that some differences exist(I can think of at least one ethnic group that is disproportionately represented in elite levels of athletic competition, for instance), discussions of the sort are quickly dismissed as racist or sexist or otherwise out of line without any further examination. Doing such hinders much academic progress in the world today.

Why should we find out if the arguments have merit when we can storm out of the room in a fit of rage, or simply shut down or switch the topic? Such responses are based on emotion, and not logic. We often hear things that are inconsistent with our beliefs. When faced with such cognitive dissonance, we often choose to discredit the opposing viewpoint even in the face of overwhelming evidence. Stifling progressive debate that we simply "don't like" is an example of this. All of this is an attempt to make it easier for us to sleep at night, assured that our beliefs about the world are correct. Facts be damned.

All of this is not to say that some of us are not truly deserving of the brands that we receive. I find, however, that such brands often are put in place for self-serving reasons... to knock someone down in a furtherance of whatever cause we champion. It is easy to imagine how things that Ron Paul might or might not have said 15 years ago may have ruffled somebody's feathers, giving someone cause to brand him as a racist and allowing us to categorically dismiss his views that are outside of the box, the boundaries of which are determined by the liberal elite. Because I know all too well how this happens, I cannot pass judgment on Ron Paul based on sensationalized snippets that were amassed for political gain. Doing so would be intellectually lazy, and completely unfair to the Senator. However, I would like to hear a credible explanation from him before I resume supporting his candidacy.

-eternitus

For what it's worth, I find it hard to believe that anyone as intelligent as he is can hold any sort of truly racist view. We know that the belief that one person is superior to another based solely on the way he or she appears can not hold up when confronted with reality.

Sunday, November 11, 2007

Ron Paul Issue of the Day: Get out of Iraq

Getting out of Iraq... The cost of the war is approaching $1 trillion, funded almost entirely by debt (debt that the boomers won't have to worry about too much, but the under-40 crowd will have to work hard at paying off). Iraq has gotten plenty of help and it's time to let them sort it out for themselves. RON PAUL IS THE ONLY REPUBLICAN CANDIDATE SUPPORTING A COMPLETE PULL OUT FROM IRAQ.

We can't afford to increase our massive national debt further by spending ruinous amounts of money carrying out an interventionist foreign policy (anyone remember what happened to those guys from Italy about 1600 years ago? You know, I think they were based in Rome...)

Ron Paul has consistently voted against the Iraq war (Hillary, eat your heart out!!!).

Saturday, November 10, 2007

I'm going to opine on political issues for a moment, even though I normally detest all things related thereto. In fact, I have been so disgusted with the choices for president in the two elections in which I was eligible to vote that I abstained from voting altogether. For once, I've found a candidate worth backing.

I'm going to opine on political issues for a moment, even though I normally detest all things related thereto. In fact, I have been so disgusted with the choices for president in the two elections in which I was eligible to vote that I abstained from voting altogether. For once, I've found a candidate worth backing.It's worth mentioning that the key issues we should be concerned with are the ones that will directly affect us. For the vast majority of Americans, their only interaction with the Federal government is the payment of taxes. On that note, I'd like to throw my support behind Senator Ron Paul for president of the United States in 2008, who supports low taxes, limited government and limited foreign intervention. I believe that he is the one candidate running today who has the right mix of competence, integrity and economic knowledge to get us out of the quagmire that we're currently in.

While he is a candidate of the Republican party, Ron Paul doesn't quite fit the Republican mold as we have come to know it recently, which now includes wasteful government spending, huge federal budget deficits and a ballooning national debt. From a generational standpoint, Senator Paul's policies, I believe, will give us non-boomers the best chance to enjoy at least a half-decent life compared to our elders.

I'll be posting Senator Paul's key platform issues, and why they're good for you, over the next few days.

- eternitus

BTW - It's only extra icing on the cake (I wouldn't vote just because of this), but Ron Paul, like eternitus, is a native Pittsburgh.

Wednesday, October 31, 2007

Feddie Krueger Cuts'em again!

OKAY.... Given that it is Halloween today, I just had to work Freddy Krueger into the mix... and the Fed has made that quite easy by slicing and dicing the federal funds rate and discount rate with all due ferocity.

Why is Mr. T in there? Well, Mr. T rules... more on that later.

Today, the Fed reduced its target federal funds rate (the rate at which banks borrow from each other) to 4.5%. How do they do this? They print money and lend to banks at 4.5% as much as is necessary to "defend" their target rate (Just trying to educate, so Mr. T does not pity you.)

All in all, I have to say that I'm in favor of the recent move, despite my distaste for artificially low interest rates, and I am most impressed with the Fed's strategic maneuvering over the last few months.

Why do I applaud their maneuvering?

First, they shocked the market in August by cutting the discount rate by 0.5%, which stopped the bleeding from August's "global margin call" or as some would call it a mini "Minsky moment." They also stepped up to the plate with loads of liquidity to make sure the credit markets didn't totally explode.

Second, the Fed cut the funds rate by a more-than-expected 0.5% in September, which (i) dramatically reduced pressure in the credit markets by lowering borrowing costs for struggling banks and making existing yields more attractive, (ii) helped sure up bank income statements due to reduced interest expense and (iii) aided interbank liquidity, continuing to ensure that the credit markets didn't totally explode.

Finally, they made sure that, after today, they wouldn't be "forced" into lowering rates again by setting proper expectations from the outset. The key phrase in their statement released today:

"The Committee judges that, after this action, the upside risks to inflation roughly balance the downside risks to growth."

This is a clear signal (as clear as you can get from the Fed) that the committee believes that, while not the case for this particular cut, any further cuts will cause inflation to become of greater concern than slow growth, meaning that they don't plan on cutting rates again unless it gets uglier out there.

BRAVO! The Fed has finally BECOME AN EFFECTIVE TOOL, moving from a reactionary implement of Chinese water torture that simply drips down the economy's forehead 0.25% at a time to a proactive hammer with the capability to shape and mold (and maybe even do a mean "typewriter"). As you see, Feddy Krueger is acting more like Mr. T and our dear friend M.C.

I have far more confidence in Bernanke than our buddy "easy Al." Greenspan's fed "Can't touch this" one.

I have far more confidence in Bernanke than our buddy "easy Al." Greenspan's fed "Can't touch this" one.Another reason why I love the rate cuts is the devaluation of the dollar. Other countries have been devaluing their currencies to prop up their economies for quite some time (instead of, you know, improving productivity or leveraging comparative advantage or investing in capital). It's about time we get to use this easy way out of economic distress. They can buy the living daylights out of our artificially cheap stuff and send all of their jobs here for once. After all, we're looking at probably 2-4 more years of housing pain... we need the help.

Will the new Fed hammer, a sizzling global economy and a sickly dollar be enough to keep us out of a recession despite years of reckless lending and misallocation of capital? Will it be able to overcome the fact that millions of debt slaves (oops, I meant "people") are being stretched thin by their retarded mortgages because they paid too much for their slowly rotting boxes (oops, I meant "homes")? I don't think so, but Bernanke, I believe, will aid in us achieving the best outcome possible given the cards we've been dealt.

Full text of the Fed's statement:

Release Date: October 31, 2007

For immediate release

The Federal Open Market Committee decided today to lower its target for the federal funds rate 25 basis points to 4-1/2 percent.

Economic growth was solid in the third quarter, and strains in financial markets have eased somewhat on balance. However, the pace of economic expansion will likely slow in the near term, partly reflecting the intensification of the housing correction. Today’s action, combined with the policy action taken in September, should help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in financial markets and promote moderate growth over time.

Readings on core inflation have improved modestly this year, but recent increases in energy and commodity prices, among other factors, may put renewed upward pressure on inflation. In this context, the Committee judges that some inflation risks remain, and it will continue to monitor inflation developments carefully.

The Committee judges that, after this action, the upside risks to inflation roughly balance the downside risks to growth. The Committee will continue to assess the effects of financial and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; Timothy F. Geithner, Vice Chairman; Charles L. Evans; Donald L. Kohn; Randall S. Kroszner;

Frederic S. Mishkin; William Poole; Eric S. Rosengren; and Kevin M. Warsh. Voting against was Thomas M. Hoenig, who preferred no change in the federal funds rate at this meeting.

Wednesday, October 24, 2007

Home Sales in Full-Fledged Rout: Disaster Continues

Courtesy of the Wall Street Journal... I guess it turns out that people really didn't plan on paying these ridiculously high mortgage payments after all. The market dried up after buyers ran out of "greater fools" to unload houses to. Oh yeah... and people actually have to pay something up-front to buy after all the piggyback (second mortgage) lenders croaked... (Can I put that 20% down-payment on my credit card?)

If you are thinking about buying - don't try and catch a falling knife - you'll probably end up with a nasty cut. Most analysts are not expecting housing to stabilize until 2009 at the earliest. The length of the "down-cycle" has a lot to do with the length of the "up-cycle," which leads me to believe that even these estimates are too optimistic. We had a 4-year boom... we may have 3 years left in a 4-year bust.

Why? Unlike stocks, people are very slow to take losses on their houses. They'll just "rent it out" until the market "comes back." These people represent "phantom inventory" that will jump into the market at the first sign of strength... creating even more downward pressure on prices. By not getting out when the can, these people end up riding the market all the way down to the bottom. To add insult to injury, they usually can't cover more than 60% of their "carrying costs" with rent, so they are losing money every month even as their house declines in value.

Let's make this another chapter in the vanquishing of the "housing tragedy" that locks young families out of homes in order to further enrich baby-boomers, whose national debt we'll have to repay in addition to funding their retirement.

If you are thinking about buying - don't try and catch a falling knife - you'll probably end up with a nasty cut. Most analysts are not expecting housing to stabilize until 2009 at the earliest. The length of the "down-cycle" has a lot to do with the length of the "up-cycle," which leads me to believe that even these estimates are too optimistic. We had a 4-year boom... we may have 3 years left in a 4-year bust.

Why? Unlike stocks, people are very slow to take losses on their houses. They'll just "rent it out" until the market "comes back." These people represent "phantom inventory" that will jump into the market at the first sign of strength... creating even more downward pressure on prices. By not getting out when the can, these people end up riding the market all the way down to the bottom. To add insult to injury, they usually can't cover more than 60% of their "carrying costs" with rent, so they are losing money every month even as their house declines in value.

Let's make this another chapter in the vanquishing of the "housing tragedy" that locks young families out of homes in order to further enrich baby-boomers, whose national debt we'll have to repay in addition to funding their retirement.

Existing-Home Sales Tumble 8%

By TOM BARKLEY

October 24, 2007 10:04 a.m.

October 24, 2007 10:04 a.m.

WASHINGTON -- Demand for previously owned homes slid more than expected in September amid continued problems in the mortgage market, with single-family sales hitting their lowest sales pace in nearly 10 years.

Overall home resales declined to a 5.04 million annual rate, an 8.0% decrease from August's downwardly revised 5.48 million annual pace, the National Association of Realtors said Wednesday.

The August existing-home sales level came in well below Wall Street expectations for a 5.25 million rate.

The 5.04 million pace is the lowest since the association started accounting for combined single family and condo sales in 1999. Based on single-family sales of 4.38 million, the September figures are the weakest since January 1998.

"The credit freeze in August definitely impacted sales in September, particularly the jumbo [loan] side, so we have seen a large sales decline in the upper end of the market," NAR senior economist Lawrence Yun said.

The median home price was $211,700 in September, down 4.2% from $220,900 in September 2006. The median price in August this year was $224,400.

Mr. Yun said conditions in the jumbo loan market have improved, so he still expects 2007 to rank as the fifth-best year in terms of existing home sales. Prices are expected to ease about 1.5% from record high of last year of $221,900.

Inventories of homes rose 0.4% at the end of September to 4.40 million available for sale, which represented a 10.5-month supply at the current sales pace. There was a 9.6 month supply at the end of August, revised down from a previously estimated 10.0 months.

Existing-home sales tumbled in all regions. Sales dropped 7.0% in the Midwest, 10.0% in the Northeast, 9.9% in the West, and 6.0% in the South.

The average 30-year mortgage rate was 6.38% in September, down from 6.57% in August, according to Freddie Mac.

Write to Tom Barkley at tom.barkley@dowjones.com

Tuesday, October 2, 2007

NAR - Worst - Ever Showing for Pending Home Sales

In another shocker, the Pending Home Sales Index released by the NAR reached its lowest point ever (even lower than September 2001).

(Click on the chart for a larger image.)

It's not too often that you see a chart (of real data) with a trend as clean as this one. According to the NAR, the problem now stems from borrowers with "good credit" who can't get loans due to the credit crunch. My only response to this is: Balderdash. As we can see, the downward trend in house sales was firmly in place before the August credit crunch.

It's not too often that you see a chart (of real data) with a trend as clean as this one. According to the NAR, the problem now stems from borrowers with "good credit" who can't get loans due to the credit crunch. My only response to this is: Balderdash. As we can see, the downward trend in house sales was firmly in place before the August credit crunch.

There is a term for this: Market Failure - when transactions cease to occur because buyers and sellers cannot come together and agree on a price.

The Buyers' Issues

Now that the Ponzi scheme is up, buyers are facing a brave new world where, if they want to buy a house, they have to:

1. Make a down payment (What is that?)

2. Pay a bloated mortgage bill for a long time (You mean this initial 2% rate is not a real mortgage rate? You mean I have to pay this back? I'm so confused!)

3. Accept subpar returns or declines in the value of their housing.

When you put it that way, forking over $35,000 for the right to pay $2,500 per month, or $30,000 per year (PITI) for a $350,000 townhouse doesn't seem so great, does it? This is especially true when you are getting a lousy return on your house because (i) you bought high and (ii) houses don't go up too much in value under normal conditions anyway.

The Sellers' Issues

This is easy. "What? I can't get the bubble price that Billy Jones got up the street? No way I'm selling for less."

Or "that's not even what I paid for my house!"

Why Prices Have to Fall Further

Eventually, something has to give. In many markets, buyers can't realistically pay the prices sellers are asking for, while a large portion of sellers (at the urging of their agents desperately trying to keep prices high) are simply being stubborn.

Time to address one "myth" commonly used to combat the notion that prices will fall materially: "Nobody will sell for less than he bought his house for."

1. Some people simply have to sell if they can't afford to pay the bills or really need to move. These people will sell for a "buyer's" price and swallow the hit to their down payment or built-up equity, busting comp sets.

2. Most importantly... not everybody bought their house in the last few years. If these sellers have to go, they'll still make a good gain if they sell for 10, 20 or even 30% below the prices they could have gotten in 2005 or 2006 (however reluctantly).

Unfortunately for sellers, their stubbornness has to yield to impossibility (buyer's inability to afford asking prices) if they want to sell their home.

Oh, and by the way, I didn't even mention that the competition for buyers is about to get a lot tougher over the next year as a new wave of inventory sweeps through the markets.

- eternitus

- eternitus

(Click on the chart for a larger image.)

It's not too often that you see a chart (of real data) with a trend as clean as this one. According to the NAR, the problem now stems from borrowers with "good credit" who can't get loans due to the credit crunch. My only response to this is: Balderdash. As we can see, the downward trend in house sales was firmly in place before the August credit crunch.

It's not too often that you see a chart (of real data) with a trend as clean as this one. According to the NAR, the problem now stems from borrowers with "good credit" who can't get loans due to the credit crunch. My only response to this is: Balderdash. As we can see, the downward trend in house sales was firmly in place before the August credit crunch.There is a term for this: Market Failure - when transactions cease to occur because buyers and sellers cannot come together and agree on a price.

The Buyers' Issues

Now that the Ponzi scheme is up, buyers are facing a brave new world where, if they want to buy a house, they have to:

1. Make a down payment (What is that?)

2. Pay a bloated mortgage bill for a long time (You mean this initial 2% rate is not a real mortgage rate? You mean I have to pay this back? I'm so confused!)

3. Accept subpar returns or declines in the value of their housing.

When you put it that way, forking over $35,000 for the right to pay $2,500 per month, or $30,000 per year (PITI) for a $350,000 townhouse doesn't seem so great, does it? This is especially true when you are getting a lousy return on your house because (i) you bought high and (ii) houses don't go up too much in value under normal conditions anyway.

The Sellers' Issues

This is easy. "What? I can't get the bubble price that Billy Jones got up the street? No way I'm selling for less."

Or "that's not even what I paid for my house!"

Why Prices Have to Fall Further

Eventually, something has to give. In many markets, buyers can't realistically pay the prices sellers are asking for, while a large portion of sellers (at the urging of their agents desperately trying to keep prices high) are simply being stubborn.

Time to address one "myth" commonly used to combat the notion that prices will fall materially: "Nobody will sell for less than he bought his house for."

1. Some people simply have to sell if they can't afford to pay the bills or really need to move. These people will sell for a "buyer's" price and swallow the hit to their down payment or built-up equity, busting comp sets.

2. Most importantly... not everybody bought their house in the last few years. If these sellers have to go, they'll still make a good gain if they sell for 10, 20 or even 30% below the prices they could have gotten in 2005 or 2006 (however reluctantly).

Unfortunately for sellers, their stubbornness has to yield to impossibility (buyer's inability to afford asking prices) if they want to sell their home.

Oh, and by the way, I didn't even mention that the competition for buyers is about to get a lot tougher over the next year as a new wave of inventory sweeps through the markets.

- eternitus

- eternitusMonday, September 24, 2007

My Beef with Greenspan: A Picture is Worth a Thousand Words

Don't you get the feeling that Alan Greenspan, in his last 5 years at the helm of the Federal Reserve, was the financial equivalent of Indiana Jones at the beginning of Raiders of the Lost Ark, with the boulder barreling after him being the over-inflated, debt-riddled Economy that he created. Like Jones, he managed to escape just in time (via retirement in Greenie's case). Boy do I feel badly for Bernanke, who is left to clean up his mess.

I have yet to read his book, but I find it amazing that Easy Al continues to downplay his role in inflating the housing bubble. He credits "low worldwide long-term interest rates" for that. He fails to mention that he set in motion the mechanism that created low long-term interest rates in the first place.

It goes something like this:

------------------------------------------------------------------------------------------------

1. Fed drops Fed Funds Rate to 1% (practically paying banks to take its money after inflation is accounted for).

2. Foreign central banks drop their target rates to preserve the dollar's value vs. their currencies (so we can keep borrowing to buy their stuff, supporting their economies).

3. Ridiculously low interest rates spur massive increase in the global money supply (money is "created" via lending - e.g...

1. Fed "creates" $10 in Open Market Operations by lending to a bank to defend its 1% Fed Funds target (without the Fed constantly buying, the lending rate would go up as banks would require higher interest rates - at least high enough to cover inflation),

2. The bank lends $7 to someone (person B) who pays person C $7 for an item.

3. Person C deposits $7 in the bank.

4. The bank lends $4 to Person D... and so on and so forth.

Just in these four steps, the Fed's $10 turns into $21 (known as the multiplier effect).

4. U.S. spends a lot of this newly created money on imports (huge trade deficit), making foreign countries RICH!

5. RICH! foreign countries invest their surpluses (paid for by our huge debt splurge) in nice, safe T-Bills, Notes and Bonds, keeping interest rates nice and low so we can continue borrowing to buy foreign goods, making foreigners RICH!

------------------------------------------------------------------------------------------------

The long and short of it: create a bunch of money, and all of that money chases the same lending opportunities. If you want to lend, you have to offer a good rate (lest the coveted borrower take someone else's monopoly money). As such, massive monetary inflation will keep rates low.

Take away Greenie's step 1., above and you don't get low long-term interest rates, a housing bubble, and most importantly this mortgage mess that Uncle Ben is trying to clean up. Uncle Ben is also trying to do this housekeeping with the politicos on the Hill trying their best to foul things up with short-sighted policy measures in order to win votes for next year's elections.

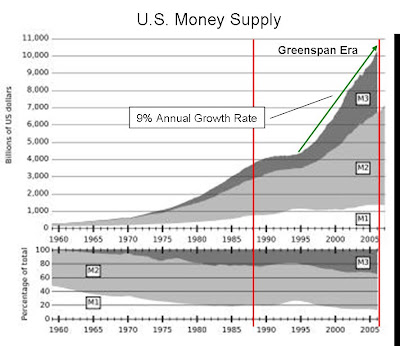

Greenspan's legacy is pretty much summed up in the following chart (click for a larger image). M3 is the broadest measure of the money supply (which the Fed conveniently stopped reporting after it completely lost control of its growth).

The Fed has aided money creation at a 9% annual rate since about 1995 - massive monetary inflation as stated above - All of that money had to go somewhere, luckily it has been in assets so far (where next?)...

Can you say... slosh - TECH BUBBLE - slosh slosh - HOUSING / CREDIT BUBBLE - slosh slosh slosh - EXPLOSIVE INFLATION? Let's hope not.

I have yet to read his book, but I find it amazing that Easy Al continues to downplay his role in inflating the housing bubble. He credits "low worldwide long-term interest rates" for that. He fails to mention that he set in motion the mechanism that created low long-term interest rates in the first place.

It goes something like this:

------------------------------------------------------------------------------------------------

1. Fed drops Fed Funds Rate to 1% (practically paying banks to take its money after inflation is accounted for).

2. Foreign central banks drop their target rates to preserve the dollar's value vs. their currencies (so we can keep borrowing to buy their stuff, supporting their economies).

3. Ridiculously low interest rates spur massive increase in the global money supply (money is "created" via lending - e.g...

1. Fed "creates" $10 in Open Market Operations by lending to a bank to defend its 1% Fed Funds target (without the Fed constantly buying, the lending rate would go up as banks would require higher interest rates - at least high enough to cover inflation),

2. The bank lends $7 to someone (person B) who pays person C $7 for an item.

3. Person C deposits $7 in the bank.

4. The bank lends $4 to Person D... and so on and so forth.

Just in these four steps, the Fed's $10 turns into $21 (known as the multiplier effect).

4. U.S. spends a lot of this newly created money on imports (huge trade deficit), making foreign countries RICH!

5. RICH! foreign countries invest their surpluses (paid for by our huge debt splurge) in nice, safe T-Bills, Notes and Bonds, keeping interest rates nice and low so we can continue borrowing to buy foreign goods, making foreigners RICH!

------------------------------------------------------------------------------------------------

The long and short of it: create a bunch of money, and all of that money chases the same lending opportunities. If you want to lend, you have to offer a good rate (lest the coveted borrower take someone else's monopoly money). As such, massive monetary inflation will keep rates low.

Take away Greenie's step 1., above and you don't get low long-term interest rates, a housing bubble, and most importantly this mortgage mess that Uncle Ben is trying to clean up. Uncle Ben is also trying to do this housekeeping with the politicos on the Hill trying their best to foul things up with short-sighted policy measures in order to win votes for next year's elections.

Greenspan's legacy is pretty much summed up in the following chart (click for a larger image). M3 is the broadest measure of the money supply (which the Fed conveniently stopped reporting after it completely lost control of its growth).

The Fed has aided money creation at a 9% annual rate since about 1995 - massive monetary inflation as stated above - All of that money had to go somewhere, luckily it has been in assets so far (where next?)...

Can you say... slosh - TECH BUBBLE - slosh slosh - HOUSING / CREDIT BUBBLE - slosh slosh slosh - EXPLOSIVE INFLATION? Let's hope not.

Friday, September 7, 2007

Great Housing Article from Seeking Alpha's Markham Lee

I have a few complaints with the methodology (he admits to them)... but his conclusions are generally sound ... a house is not, nor has it ever been, quite the investment you think it is.

-eternitus

-eternitus

Adjusted Case Schiller Housing Data

After reading an article from a fellow Seeking Alpha contributor with Case-Schiller housing appreciation data for the 1990s and for the ‘00s thru May of this year, I began to wonder how the data would look if:

Friday, August 17, 2007

NEVER.... SELL... INTO.... A.... PANIC!!!! THAT IS SHAMEFUL!

Unless you really have to (as in a margin call)....

Waiting one day for the panic to subside is worth about 5.5% in this case, or the amount of money you could earn on a 12-month CD, or $550 on every $10,000 invested.

By the way, I'm on vacation this week. Are you jealous?

See you in a week (or on the other side).

See you in a week (or on the other side).

-eternitus

Waiting one day for the panic to subside is worth about 5.5% in this case, or the amount of money you could earn on a 12-month CD, or $550 on every $10,000 invested.

By the way, I'm on vacation this week. Are you jealous?

See you in a week (or on the other side).

See you in a week (or on the other side).-eternitus

Thursday, August 9, 2007

OMG! The stock market can go DOWN!?!?!?! - A little advice from an investment pro

A good stock chart can tell a great story... as does the chart below depicting the S&P 500 over the last year.

Click on the chart for a larger image.

Apart from being a great reminder that the market is really just a bunch of scared, greedy people buying and selling... this chart is a prime example of why most small-time investors (as I presume you are) underperform the pros by a significant margin. We all want to buy after we've seen "YAY!" for a while (for fear of missing out) and sell immediately in times of trouble (usually a few days after a big drop, when we don't see a rebound).

Guess what? The guys who make the real money in the markets do the opposite. They buy when you soil your pants and give your shares away at bargain basement prices, and they sell to you when you want to jump on the bandwagon.

This is why I'm buying now, as I did in early March. Lot's of good stocks fall for no reason other than blind fear. The key is separating the wheat from the chaff.

Oh, and remember... there is a difference between price and value... every stock has one value, but many prices.

Click on the chart for a larger image.

Apart from being a great reminder that the market is really just a bunch of scared, greedy people buying and selling... this chart is a prime example of why most small-time investors (as I presume you are) underperform the pros by a significant margin. We all want to buy after we've seen "YAY!" for a while (for fear of missing out) and sell immediately in times of trouble (usually a few days after a big drop, when we don't see a rebound).

Guess what? The guys who make the real money in the markets do the opposite. They buy when you soil your pants and give your shares away at bargain basement prices, and they sell to you when you want to jump on the bandwagon.

This is why I'm buying now, as I did in early March. Lot's of good stocks fall for no reason other than blind fear. The key is separating the wheat from the chaff.

Oh, and remember... there is a difference between price and value... every stock has one value, but many prices.

Tuesday, July 31, 2007

Wednesday, July 11, 2007

Thought of the Day...

The media did make a fuss about this May's abysmal pending home sales report (So I have to give them credit for that). However, they glossed over one key point. Read:

-----------------

The National Association of Realtors said its Pending Home Sales Index, based on contracts signed in May, fell 3.5 percent to 97.7 from a downwardly revised level of 101.2 in April. The May index is the lowest since 89.8 in September 2001. via the International Business Times -.

-------------

Um... didn't something really bad happen in September 2001? I can't quite put my finger on it...

Oh yeah... that 9/11 thing...

I mean, it's really, really, really bad when the only month you can find worse is the one where our country was attacked, thousands of people died and billions of dollars of damage was caused.

- eternitus

-----------------

The National Association of Realtors said its Pending Home Sales Index, based on contracts signed in May, fell 3.5 percent to 97.7 from a downwardly revised level of 101.2 in April. The May index is the lowest since 89.8 in September 2001. via the International Business Times -.

-------------

Um... didn't something really bad happen in September 2001? I can't quite put my finger on it...

Oh yeah... that 9/11 thing...

I mean, it's really, really, really bad when the only month you can find worse is the one where our country was attacked, thousands of people died and billions of dollars of damage was caused.

- eternitus

Wednesday, July 4, 2007

What a great fourth of July Present

I was able to borrow an internet connection for this short post...

Just in case you're the one guy who thinks everything is on the up and up in the public markets... This was written before Blackstone's announcement that it was taking the Company private.

----------------------------------------------------------------------------------------------

Insider trading in stocks is one thing. However, when you're knowingly trading with insider information in options, you're really ripping someone off.

That's because options involve an agreement between two parties. Let's examine...

Johnny Insider - He's the brother of an analyst at Blackstone Group. His sister - Lucy Lips, the analyst, lets the cat out of the bag that Blackstone agreed to buy Hilton at $47.50, more than $13.00 greater than the current price on the market on July 3. Johnny has $10,000 to spare, and is looking to use this information to his advantage. He has two choices - buy approximately 200 shares of Hilton, which would make him $2,600... or he could use the implied leverage of options, and make 20 times that much (you'll see how in a bit)...

Honest George - He's a market maker in options - market makers provide a valuable service... constantly offering to buy and sell shares at certain prices, giving all of us liquidity. He doesn't have any insider information, and believes that Hilton shares aren't going above $40.00 any time soon. He decides to sell the right to purchase 10,000 Hilton shares at $40.00 per share before the end of August for $1.00 per share.

He's selling a call option... As a recap, the buyer (Johnny) pays a "premium" $1.00 to the seller (George) for the right to purchase the shares at a specified price ($40.00).

Initially, Johnny pays George $10,000... which George believes to be fair compensation for the possibility that the shares will exceed $40.00, which would mean that he'd have to buy them at the higher market price and sell them to Johnny for a loss. Unfortunately, Johnny knows something George does not.

Tomorrow, Hilton's market price will skyrocket to $47.50 and Johnny will exercise his options. This means that George will have to pay $475,000 for 10,000 shares of Hilton and then sell them to Johnny for $400,000, taking a $65,000 loss (the $10,000 premium offsets some of the loss). Johnny can now sell his shares at the market price, netting a $65,000 gain(he doesn't get the premium back. As you see... the options strategy is far more profitable than simply buying shares...

Now you see how Johnny ripped George off.

George is a market maker, so it's his company's money he's losing. $65,000 doesn't seem like a big deal... but George makes tens of thousands of these transactions per day.... His trading strategy is supposed to be "market neutral"... meaning that he should make small amounts of money on each trade if the market goes either way. However, such a strategy only works when you know as much as everyone else does. George's exposure to loss may have reached into the millions before he got wise, costing the investors in his company (Average joes who invest in Goldman, Interactive Brokers Group, etc.) tons of money and putting his job in jeopardy.

I hope the SEC finds every one of the "Johnny's" out there. We all deserve a level field when we're trading in the markets.

- eternitus

Just in case you're the one guy who thinks everything is on the up and up in the public markets... This was written before Blackstone's announcement that it was taking the Company private.

----------------------------------------------------------------------------------------------

The market looks to be positioning for volatile price action at Hilton Hotels Corp (HLT), where upwards of 32,000 lots moved today in options trading – 15 times the daily average volume for the hotel chain. While twice as many calls as puts moved today, concentrations of volume favored the July and August 35.0 straddles, and the July and August 40.0 calls.

The abrupt increase in volatility positioning indicates that the market is bracing for turbulence in Hilton shares with an uncertain, upside bias. Hilton shares gained 7 percent today to close at $36.10 in heavy trading – and with no market-moving news of note, we wonder if there' something to the chatter. Implied volatility on Hilton options soared 20 percent and currently sits at just above 38 percent – significantly above the 25 percent recorded historical volatility on Hilton shares.

------------------------------------------------------------------------------------------------Insider trading in stocks is one thing. However, when you're knowingly trading with insider information in options, you're really ripping someone off.

That's because options involve an agreement between two parties. Let's examine...

Johnny Insider - He's the brother of an analyst at Blackstone Group. His sister - Lucy Lips, the analyst, lets the cat out of the bag that Blackstone agreed to buy Hilton at $47.50, more than $13.00 greater than the current price on the market on July 3. Johnny has $10,000 to spare, and is looking to use this information to his advantage. He has two choices - buy approximately 200 shares of Hilton, which would make him $2,600... or he could use the implied leverage of options, and make 20 times that much (you'll see how in a bit)...

Honest George - He's a market maker in options - market makers provide a valuable service... constantly offering to buy and sell shares at certain prices, giving all of us liquidity. He doesn't have any insider information, and believes that Hilton shares aren't going above $40.00 any time soon. He decides to sell the right to purchase 10,000 Hilton shares at $40.00 per share before the end of August for $1.00 per share.

He's selling a call option... As a recap, the buyer (Johnny) pays a "premium" $1.00 to the seller (George) for the right to purchase the shares at a specified price ($40.00).

Initially, Johnny pays George $10,000... which George believes to be fair compensation for the possibility that the shares will exceed $40.00, which would mean that he'd have to buy them at the higher market price and sell them to Johnny for a loss. Unfortunately, Johnny knows something George does not.

Tomorrow, Hilton's market price will skyrocket to $47.50 and Johnny will exercise his options. This means that George will have to pay $475,000 for 10,000 shares of Hilton and then sell them to Johnny for $400,000, taking a $65,000 loss (the $10,000 premium offsets some of the loss). Johnny can now sell his shares at the market price, netting a $65,000 gain(he doesn't get the premium back. As you see... the options strategy is far more profitable than simply buying shares...

Now you see how Johnny ripped George off.

George is a market maker, so it's his company's money he's losing. $65,000 doesn't seem like a big deal... but George makes tens of thousands of these transactions per day.... His trading strategy is supposed to be "market neutral"... meaning that he should make small amounts of money on each trade if the market goes either way. However, such a strategy only works when you know as much as everyone else does. George's exposure to loss may have reached into the millions before he got wise, costing the investors in his company (Average joes who invest in Goldman, Interactive Brokers Group, etc.) tons of money and putting his job in jeopardy.

I hope the SEC finds every one of the "Johnny's" out there. We all deserve a level field when we're trading in the markets.

- eternitus

Monday, June 25, 2007

Blogger Without an Internet

Not only was I overwhelmed with things to do over the past few weeks... When I finally got the chance to sit down and write something, I find that I no longer have a functioning internet at home... I won't until Thursday at the earliest. I'm putting in a quick post from work now just to let the readers out there know I'm still kicking...

Be on the lookout for another horrid existing home sales number today, which may again show price declines. If not... be fairly sure that it's just a blip.

After I get the long-promised big post on housing out of the way, hopefully this weekend... we'll talk stocks, and why everyone who's going to be alive for more than 20 years longer should hold them in some form (and can withstand the occasional large drop in value because he / she doesn't need to use the money immediately).

Be on the lookout for another horrid existing home sales number today, which may again show price declines. If not... be fairly sure that it's just a blip.

After I get the long-promised big post on housing out of the way, hopefully this weekend... we'll talk stocks, and why everyone who's going to be alive for more than 20 years longer should hold them in some form (and can withstand the occasional large drop in value because he / she doesn't need to use the money immediately).

Thursday, June 7, 2007

What? Inflation?

I love this guy...

You see, we have been living in a benign non-inflationary environment, and just yesterday, it seems that some traders have discovered that -- WTF?! -- prices of goods and services are rising.

Of course, many pundits, traders and investors -- and a goodly part of the Federal Reserve -- have convinced themselves that there really wasn't any inflation, so long as we wear blinders and ignore those pesky goods and services like Food and Energy. You know, those annoying items utterly necessary for survival.

That's been the f@#ktard explanation, anyway. If you believe it, though, you must be living in a cave -- which given the market for bat guano and stalagmites, probably has achieved the elusive Fed goal of price stability.

Bill King notes that:

For April 2007, the monthly food cost is $1044.80 for average family of four, per the USDA.

For April 2006, the monthly food cost is $995.40 for average family of four. Ergo y/y food inflation is 4.963% according to the USDA.

The BLS has ‘food’ inflation (urban) at only 3.7% y/y (unadjusted) for April 2007. Ergo, there is a 34% discrepancy in food inflation reporting between U.S. Government Agencies – the USDA and BLS.

This story from May 24, 2007 went largely unnoticed: Reuters reports, “The Federal Reserve's adherence to core inflation, which strips out food and energy prices, is taxing the public's patience and risks credibility, a senior U.S. central banker said on Thursday.‘In the United States over the last 20 years, core measures excluding food and energy did take out a lot of noise. But in the last three years it has been extracting quite a bit of signal,’ said Harvey Rosenblum, head of research at the Federal Reserve Bank of Dallas.”

Meanwhile, the rest of the world continues to raise their interest rates to fight inflation.

~~~

The Chicago Sun-Times was kind enough to include this table of food price increases:

Here's a sampling of where food prices are heading across the nation:

| National average prices | April 2007 | April 2002 | April 1997 |

| White bread (pound) | $1.20 | $1.00 | $.86 |

| Ground beef (pound) | $2.25 | $1.78 | $1.38 |

| Bacon (pound) | $3.50 | $3.26 | $2.66 |

| Whole chicken (pound) | $1.12 | $1.11 | $1.00 |

| Eggs (dozen) | $1.62 | $1.05 | $1.08 |

| Milk (gallon) | $3.14 | $2.78 | $2.61 |

| Butter (pound) | $2.86 | $3.20 | $2.18 |

| Ice cream (half gallon) | $3.79 | $3.72 | $2.90 |

| Red delicious apples (pound) | $1.10 | $.91 | $.90 |

| Bananas (pound) | $.52 | $.50 | $.52 |

| Navel oranges (pound) | $1.24 | $.75 | $.60 |

| Iceberg lettuce (pound) | $.99 | $1.15 | $.67 |

| Tomatoes (pound) | $1.63 | $1.32 | $1.35 |

| Frozen orange juice (12 oz.) | $2.52 | $1.89 | $1.73 |

| Sugar (pound) | $.51 | $.44 | $.44 |

| Peanut butter (pound) | $1.75 | $1.98 | $1.81 |

| Coffee, ground roast (pound) | $3.44 | $2.98 | $3.89 |

| Potato chips (16 oz.) | $3.48 | $3.29 | $3.18 |

Source: U.S. Department of Labor, Bureau of Labor Statistics

Tuesday, June 5, 2007

Ron Paul for President - A better America in 2008

I'm going to opine on political issues for a moment, even though I normally detest all things related thereto. In fact, I have been so disgusted with the choices for president in the two elections in which I was eligible to vote that I abstained from voting altogether. For once, I've found a candidate worth backing.It's worth mentioning that the key issues we should be concerned with are the ones that will directly affect us. For the vast majority of Americans, their only interaction with the Federal government is the payment of taxes. On that note, I'd like to throw my support behind Senator Ron Paul for president of the United States in 2008, who supports low taxes, limited government and limited foreign intervention. I believe that he is the one candidate running today who has the right mix of competence, integrity and economic knowledge to get us out of the quagmire that we're currently in.

While he is a candidate of the Republican party, Ron Paul doesn't quite fit the Republican mold as we have come to know it recently, which now includes wasteful government spending, huge federal budget deficits and a ballooning national debt. From a generational standpoint, Mr. Paul's policies, I believe, will give us non-boomers the best chance to enjoy at least a half-decent life compared to our elders.

Some of his key platform points are below:

Getting out of Iraq... The cost of the war is approaching $1 trillion, funded almost entirely by debt (debt that the boomers won't have to worry about too much, but the under-40 crowd will have to work paying off). Iraq has gotten plenty of help and it's time to let them sort it out for themselves. RON PAUL IS THE ONLY REPUBLICAN CANDIDATE SUPPORTING A COMPLETE PULL OUT FROM IRAQ.

We can't afford to increase our massive national debt further by spending ruinous amounts of money carrying out an interventionist foreign policy (anyone remember what happened to those guys from Italy about 1600 years ago? You know, I think they were based in Rome...)

Ron Paul has consistently voted against the Iraq war (Hillary, eat your heart out!!!).

Limited Government.. "I believe in limited government. The purpose of government is to protect liberty and not to run our lives or run the economy or police the world." - Ron Paul