Laura Rowley Money & Happiness

Has the American Dream Become a Fairy Tale?

by Laura Rowley

Once upon a time there was a greedy young man with shiny wingtips and important degrees. His father, an advisor to the king, had paid the young man's way through an Ivy League college and got him a job managing the village's pension investments.

The greedy young man went to his magic mirror and said, "Mirror, mirror, I'm at the top of my field, I'm entitled to a higher yield. I'd like to earn that yield today, so I get a bonus with my pay. Tell me now, because here's the thing -- I'm really entitled to earn more than the king."

The mirror replied, "Call Wall Street please, and invest in mortgage-backed securities. Don't worry whether the yield will last, this way you'll get your bonus fast."

And the greedy young man went on television, where the media declared him a genius.

The Investment Banker

Once upon a time there was a greedy investment banker with shiny high heels and important Ivy League degrees. She went to her magic mirror and said, "Mirror, mirror on the wall, I'm clearly entitled to a windfall. I'm putting upon you the onus -- what's the best way to boost my bonus?"

The mirror replied, "Here you'll find the recipe -- sell this hot security: Bundle good and bad mortgages together, slice and dice them and sell them as treasure. Don't worry about what's really inside -- anything foul the rating agencies can hide. If you follow my advice today, surely you'll increase your rate of pay."

And the greedy investment banker went on television, where the media declared her a genius.

The Bank President

Once upon a time there was a greedy bank president with a fancy gold watch and important degrees. He went to his magic mirror and said, "I find myself on the executive floor -- I'm really entitled to be earning more. If the stock went up I'd have no cares, since I own about a million shares. Ten other banks have opened on my block -- tell me how to boost my stock."

The mirror replied, "Hand out mortgages across the land, and sell them to Wall Street as fast as you can. Heed my word in this endeavor, and your stock will go up and up forever."

And the greedy bank president went on television, where the media declared that his bank's stock would likely go up forever.

The Mortgage Broker

Once upon a time there was a greedy young man with a not-so-fancy degree and a leased Porsche. He went to his magic mirror and said, "Mirror, mirror, I want to be rich, tell me where I can find my niche. I've read 'The Secret' and I'm ready for action, I'm familiar with the laws of attraction. My ambition is so thoroughly unbridled, I think you'll agree that I'm entitled."

The mirror replied, "Now my friend don't fret or frown, but make some loans with no money down. Become a mortgage broker and get on the phone; get some expertise in the 'liar loan.' Find suckers with no income to sign on the line, tell them when the rate adjusts things will be fine. Or sign yourself, who needs permission? Just make sure the loan has the biggest commission. Since you're lending the bank's money there's no hitch, just close those loans and you'll be rich."

And the mortgage broker went on television, where he starred in a commercial as Crazy Morty the Mortgage Broker, urging would-be homeowners to call him at 1-800-555-4567.

The Greedy Townsperson

Once upon a time there was a greedy townsperson who lived in his parents' basement and spent most of his time watching television. He saw the mortgage broker's commercial, went to his magic mirror, and said, "I don't have a job or a fancy degree, but I'm smarter than those geniuses on TV and I'm entitled to a home for free. Should I call the number that I see?" And the mirror replied, "Yes, and then cash out your equity."

He bought a McMansion and, six months later, cashed out the equity and bought a Lexus.

The Hard-Working Townsperson

Once upon a time there was a hardworking townsperson, the neighbor of the man who bought the McMansion. The hardworking man toiled in IT for the bank, where he received raises of 4 percent a year. Unfortunately, his expenses -- food, gas, utilities, taxes, health insurance, college tuition, even the cleats for his kids' soccer shoes -- were rising much faster. He drove an 8-year-old minivan, and had scrimped and saved to buy a house he could afford -- even putting 20 percent down.

He went to his magic mirror and said, "Mirror, mirror, I'm exhausted. Today at work I almost lost it. I come home from my toil and fall into bed. What can I do to get ahead?" And the mirror replied, "I have no schemes for such an honest dude -- I sincerely hope you don't get screwed."

The Moral

And as it turned out, the mortgage-backed securities were not treasure, and the pension fund went broke. The king made up for the loss by doubling taxes. The greedy young man and the greedy investment banker both got lucrative new jobs at a hedge fund run by an Ivy League pal.

The bank stock didn't go up forever -- it crashed to $5 a share -- but the bank president received a bailout worth $160 million and retired to the Caribbean. The mortgage broker moved to the Caribbean as well, where he was recognized by the banker who had enjoyed his Crazy Morty TV commercials. The banker got him a job running the country club's caddy shack.

The townsperson who bought the McMansion couldn't afford his mortgage when the rate reset, so the government bailed him out. The hardworking townsperson was laid off with no severance (that money had been given to the bank president). The hardworking townsperson's home plunged in value and his taxes went up (to bail out his neighbor and the kingdom's pension fund). His IT job was sent overseas, where the bank hired a programmer for $8,000 a year.

And the mirror just sighed at all the trouble. "Another mania, another bubble. The winners get out before it bursts, the man who follows the rules is cursed. With a sense of entitlement and plenty of greed, you can win this game with lightning speed. I've told the tale, and now I'm finished."

And the American Dream was greatly diminished.

![[Hillary's Bad History]](http://s.wsj.net/public/resources/images/AG-AA869_1japan_20080330205420.gif)

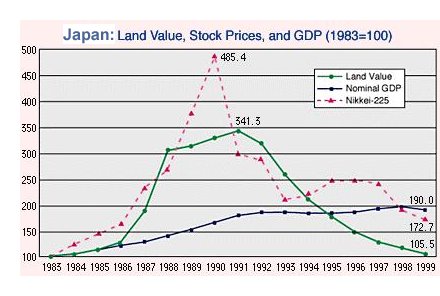

That means real estate slumps tend to grind on for years, until sellers submit to reality and reduce their prices.

That means real estate slumps tend to grind on for years, until sellers submit to reality and reduce their prices.

![[Ben Bernanke]](http://s.wsj.net/public/resources/images/HC-GG945_Bernan_20070329150953.gif)